INTRODUCTION

As Carney (2015) points out, even the destructive effects of climate change already being observed today may appear modest when compared with potential future shocks, which may have global consequences for food security, access to water, migration, and political stability.

For precisely this reason, an increasing number of central banks around the world recognise the need to develop tools that enable a more accurate assessment of climate risks and their potential impact on financial stability. One of the key instruments in this regard is climate-risk stress testing, which essentially represents a scenario-based analysis of extreme climate events or abrupt policy changes designed to simulate their effects on the banking, financial, and broader economic sectors of a country.

Advanced economies, including euro-area countries, the United States, and the United Kingdom, have already begun implementing such instruments, whereas most developing countries, including Montenegro, have not yet established adequate methodological frameworks.

1. LITERATURE REVIEW

Recent research has paid particular attention to the impact of climate risks on banks’ asset quality, especially through the non-performing loans (NPL) indicator. Evidence from European Union countries suggests that greater exposure to physical climate risks leads to a statistically significant increase in the share of NPLs in total credit portfolios (Delis et al. 2024). Similar results are reported in a study by the Central Bank of Mexico, which shows that chronic physical risks may cause losses exceeding 35% of GDP by the end of the century, with the financial sector being particularly affected through the deterioration of borrowers’ repayment capacity (Estrada et al. 2024).

The adverse impact of rising NPLs on macroeconomic indicators, particularly GDP growth, has been confirmed in several studies. According to Klein (2013), a higher share of non-performing loans negatively affects economic growth because banks reduce lending activity, which in turn lowers investment and consumption. The same effect was observed by Louzis, Vouldis, and Metaxas (2011), who used a dynamic panel model to analyse peripheral euro-area economies. Messai and Jouini (2013) further emphasise that GDP growth is negatively associated with NPLs, while unemployment and real interest rates are positively associated with the growth of non-performing loans.

At the same time, an increase in the level of NPLs directly affects banks’ capital adequacy, which may threaten financial stability. A World Bank study (2024) found that a chronic physical shock, such as drought, may reduce the CAR by an average of about 2.2 percentage points over a five-year simulation horizon, while extreme floods reduce CAR by approximately 0.14 percentage points per year on average.

2. THEORETICAL AND CONCEPTUAL FRAMEWORK

In the economic literature, climate risks are typically divided into three broad categories: physical risks, transition risks, and, increasingly, liability risks (Campiglio et al. 2018; Zhou et al. 2023). Physical risks arise from more frequent and more intense extreme weather events, such as floods, droughts, hurricanes, and fires. These events directly affect the real economy, reduce the value of assets, and threaten loan repayment. Transition risks, by contrast, arise from the process of economic adjustment and the shift towards a green economy. They include policy, regulatory, and technological changes that may disrupt the stability of existing business models. The third dimension of climate risk, liability risk, refers to the legal and financial consequences that may arise if institutions, firms, or states are held responsible for environmental damage (Zhou et al. 2023).

The financial system has proven particularly vulnerable to climate risks because these risks threaten not only individual institutions but also the systemic coherence of the entire sector. Insurance companies, as financial intermediaries, are directly exposed to physical risks and have already recorded significant losses resulting from increasingly severe natural disasters. This study therefore starts from physical risks and examines how such an event may be transmitted through different financial and economic institutions and affect the welfare of a country.

To achieve this, it is necessary to develop a reliable methodological framework for climate-risk stress testing, tailored to the specific characteristics of the national financial system and institutional architecture.

3. RESEARCH METHODOLOGY

This paper applies a quantitative approach that combines regression analysis and scenario simulation, focusing on a physical risk, specifically the 2010 flood, which was recorded as the most destructive climate-related event in the recent history of Montenegro and whose consequences may significantly affect the financial system through various channels. A quasi top-down model was selected to analyse the relationship between a climate shock and credit risk through non-performing loans (NPLs), while controlling for macroeconomic variables such as inflation and unemployment.

3.1 Defining the Climate Stress-Test Model

This study applies a simplified quantitative climate stress-test model in order to assess the effect of a physical climate risk, specifically a flood, on the financial stability of Montenegro. The model is inspired by approaches used by the European Central Bank (ECB) and the Network for Greening the Financial System (NGFS), but it is adapted to the available macroeconomic data and the specific characteristics of the domestic financial system.

The share of non-performing loans (NPLs) was selected as the main indicator of financial-system sensitivity, as it measures credit risk and banking-sector resilience. The regression model is specified so that NPLs depend on a climate shock (a flood dummy variable), the inflation rate (to account for price-stability effects), and the unemployment rate (as an indicator of financial pressure on households and their capacity to repay debt). This model enables the isolation of the effect of the climate event, i.e. the 2010 floods that affected Montenegro, while controlling for macroeconomic factors that traditionally influence the growth of credit risk.

After analysing the available data and relevant sources, including the EM-DAT database and national statistics, 2010 was identified as the year in which Montenegro experienced the most severe flood in the last two decades. This event caused widespread consequences, including damage to housing, agriculture, and infrastructure, as well as measurable fiscal costs and effects on households’ creditworthiness. For this reason, the dummy variable (flood_dummy) takes the value of 1 only for 2010, while it is set to 0 for all other years.

The data were collected from the websites of the Statistical Office of Montenegro (MONSTAT) and the World Bank for all available years, covering the period from 2007 to 2023. The regression model is presented in Table 1. The model was estimated using robust standard errors due to the small sample size and potential heteroskedasticity (Imbens and Kolesár 2016).

Source: Created by the author

| Linear regression | Number of observations | = | 17 | ||

| F (2, 13) | = | . | |||

| Prob. > F | = | . | |||

| R2 | = | 0.4944 | |||

| Root MSE | = | 4.594 | |||

| Variable | Coefficient | Robust std. error | t | P>|t| | 95% confidence interval |

| flood_dummy | 6.6466 | 2.6239 | 2.53 | 0.025 | 0.9778 to 12.315 |

| inflation | -0.0875 | 0.2733 | -0.32 | 0.754 | -0.6779 to 0.5028 |

| unemployment | 1.5659 | 0.6981 | 2.24 | 0.043 | 0.0577 to 3.0741 |

| constant | -16.2989 | 11.9812 | -1.36 | 0.197 | -42.1828 to 9.5849 |

The model shows that the 2010 flood had a statistically significant effect on the increase in the share of non-performing loans, amounting to 6.65 percentage points. This finding indicates a high degree of banking-sector sensitivity to physical climate risks and provides the basis for further stress testing. Inflation did not prove to be a statistically relevant variable, whereas unemployment has a positive and significant effect on NPLs, which is consistent with expectations: an increase in unemployment reduces borrowers’ repayment capacity. The model’s coefficient of determination is 0.49, indicating that the model explains approximately 49% of the total variability in the share of non-performing loans. Although this does not represent a high degree of explanatory power, the value is satisfactory for econometric analyses based on a limited number of observations and macroeconomic data that are often subject to numerous external influences not included in the model.

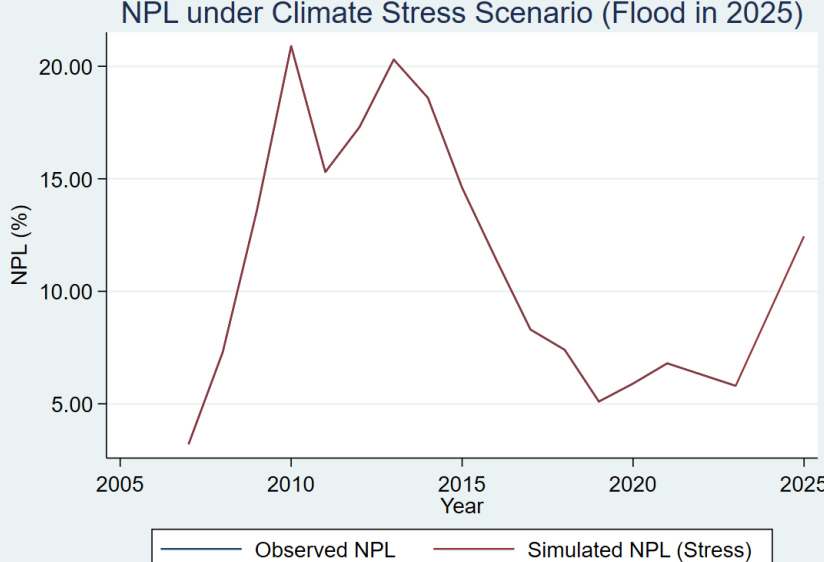

Based on the estimated flood effect on NPLs, a stress scenario was constructed in which a similar event is simulated for 2025. Under this scenario, the share of NPLs is assumed to increase by 6.65 percentage points relative to the 2023 value of 5.8%, producing a projected level of 12.45% for 2025. This implies a doubling of exposure to credit risk, with likely implications for banks’ capital adequacy, liquidity, and macro-financial stability.

Source: Created by the author

The following section assesses the estimated effect of this shock on the GDP growth rate and on capital adequacy (CAR) in Montenegro for the same year.

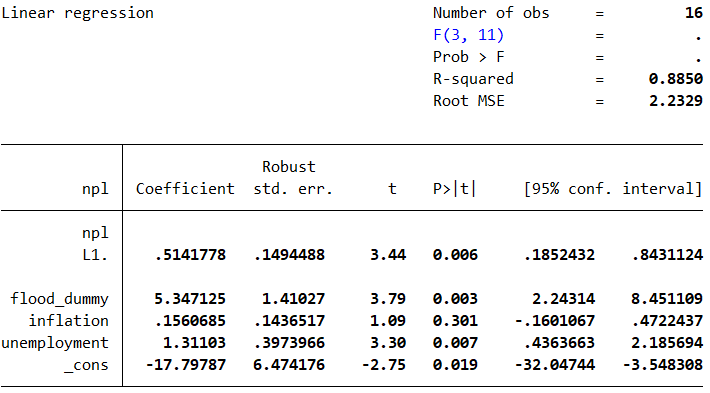

The analysis was additionally strengthened by conducting a bootstrap regression and by estimating a lagged NPL regression model. Including the lagged level of NPLs makes it possible to control for the effect of past values on the current level of credit risk, thereby reducing the omitted-variable problem and producing a more precise estimate of the actual impact of floods on the quality of banks’ loan portfolios. The extended dynamic model that includes lagged NPLs confirms the persistence of credit risk and the stability of the flood effect (Appendix 1).

To test the robustness of the baseline model, a bootstrap regression with 1,000 replications was conducted; it did not change the significance of the main coefficients.

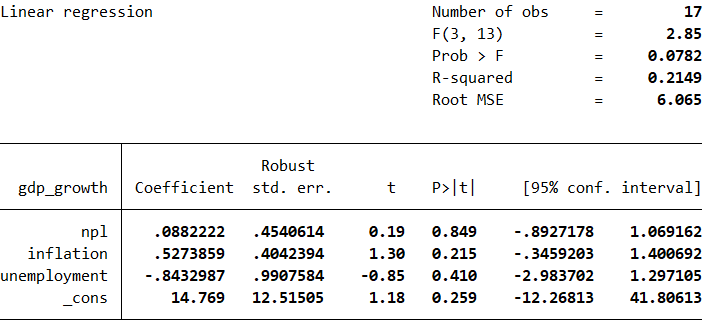

One of the key steps in the analysis was to use a quantitative model to examine how a climate shock, specifically a major flood, may affect the financial and macroeconomic stability of Montenegro. For this purpose, a regression model was formulated in which the GDP growth rate is the dependent variable, while the share of non-performing loans (NPLs), inflation, and unemployment are used as independent variables. To avoid overburdening the main text, the model is presented in Appendix 2.

This approach is consistent with the recommendations of several central banks and research institutions that use similar methods to better understand the potential macroeconomic effects of climate shocks (NGFS 2020; ECB 2021).

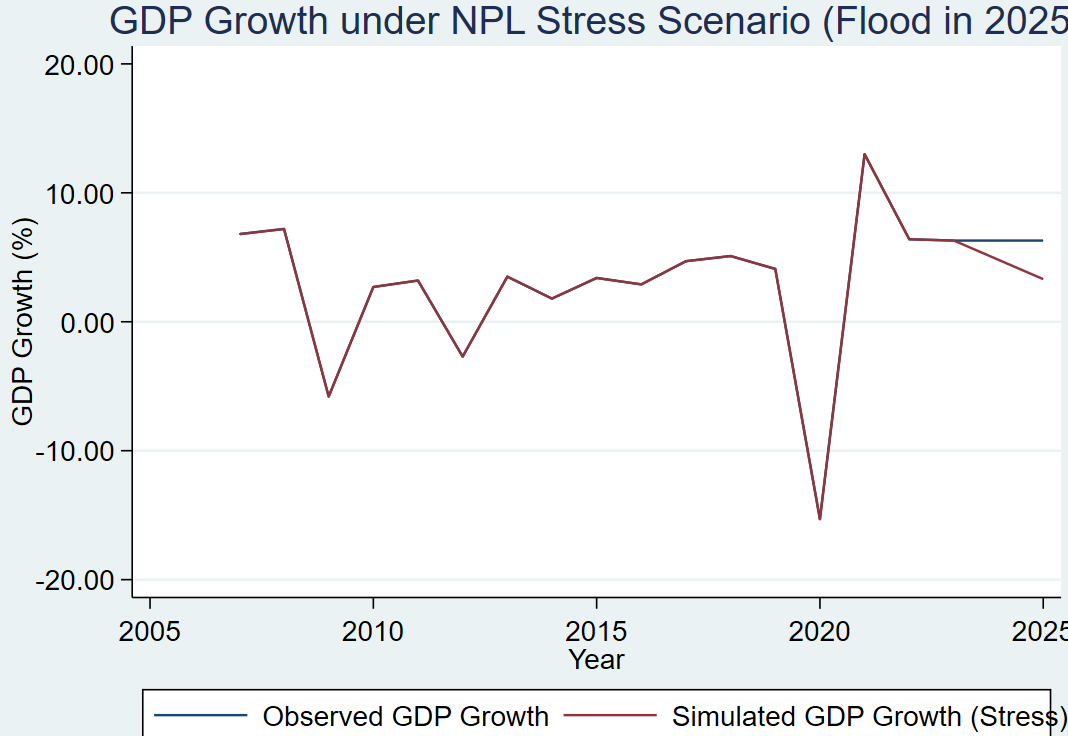

Specifically, the assumed physical climate shock, an extreme flood in 2025, was simulated through an increase in the share of non-performing loans from 5.8% to 12.45%, representing a shock of 6.65 percentage points. Based on the previously estimated relationship between NPLs and GDP growth, it was calculated that such an increase in NPLs could reduce the GDP growth rate in 2025 by approximately 0.54 percentage points.

Source: Created by the author

Figure 2 shows the difference between the projected GDP path without the shock (blue line) and the simulated growth rate in the case of a climate shock affecting the financial sector (red line). The deviation in 2025 visually confirms the simulation results and points to the serious consequences that may arise from physical climate shocks. It should be noted, however, that the analysis is based on the 2010 scenario, whereas future climate-related disasters may be considerably more severe.

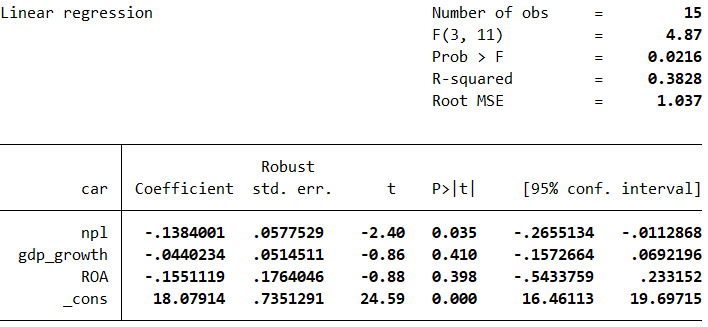

In the final step of the analysis, attention was directed to banking-system stability, specifically to how a climate shock may affect banks’ capital adequacy ratio (CAR), one of the key indicators of banking-sector resilience. For this purpose, a linear regression model was used in which CAR is specified as the dependent variable, while the share of non-performing loans (NPLs), the GDP growth rate, and return on assets (ROA), which reflects bank profitability, are included as independent variables (Appendix 3). The data were collected from the World Bank website and cover the period from 2007 to 2023, except for ROA, for which the latest available data refer to 2021.

The model results indicate a statistically significant negative relationship between NPLs and CAR: an increase in the share of non-performing loans by one percentage point leads to an approximately 0.14 percentage-point decrease in capital adequacy (p = 0.035). Although the remaining variables in the model did not show statistical significance, they were retained for control purposes and to provide a more comprehensive view of the structure of effects.

The decline in CAR results from increased provisioning and the growth of risk-weighted assets, which is consistent with standard regulatory mechanisms.

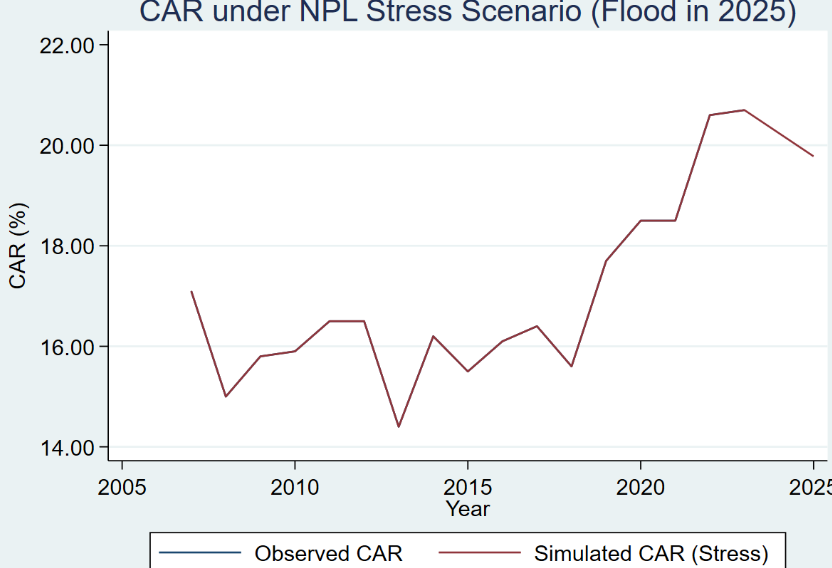

Based on this model, a climate-shock scenario simulation was conducted in which an extreme flood in 2025 is assumed to cause a sharp increase in NPLs. Applying the estimated model, the path of CAR was simulated under these conditions, making it possible to assess the potential effects of climate risk on bank capital.

Source: Created by the author

Figure 3 presents the simulated CAR path under the climate-shock scenario (red line), showing a clear decline in 2025 relative to the previous trend. This visually confirms the model results and highlights the importance of integrating climate risks into financial-stability assessments, as the spillover effect of climate shocks, in this case physical shocks, on the macro-financial profile of an economy is evident.

Although these are basic models for climate-shock stress testing, the results indicate potentially significant and systemic implications of climate events for banks’ capital positions. For this reason, such simulations serve as a starting point for further development of climate stress testing and as support for policymakers in defining macroprudential measures and managing climate risks in line with the growing requirements of international regulators such as the NGFS (2020) and the BIS (2021).

The climate stress-test model implemented in this study is not limited to direct physical risk, but also models its systemic effects throughout the financial chain: from bank balance sheets, through the real economy, to sectoral capital stability. The methodology applied allows for a relatively simple, yet analytically convincing, simulation of climate risk tailored to the Montenegrin context and provides a basis for the further development of more advanced stress-testing exercises within the Central Bank or other regulatory authorities.

3.2 Diagnostic Tests

The diagnostic tests relevant to this analysis include tests of stationarity, heteroskedasticity, autocorrelation, and multicollinearity. The Augmented Dickey-Fuller (ADF) test was used to examine stationarity, and the results are presented in the table below at the 5% level of statistical significance.

Source: Created by the author

| Variable | Level (ADF) | First difference (ADF) | Conclusion |

| NPL | Non-stationary | Stationary | I(1) |

| Inflation | Non-stationary | Stationary | I(1) |

| Unemployment | Non-stationary | Stationary | I(1) |

| CAR | Non-stationary | Stationary | I(1) |

| GDP growth rate | Stationary | — | I(0) |

To examine the existence of a long-run relationship between the observed variables, residual-based tests were conducted. The results indicate the presence of cointegration, which justifies estimating the model in levels. None of the diagnostic tests indicated serious econometric problems, while robust standard errors were used to increase the reliability of the estimates.

3.3 Discussion of Results

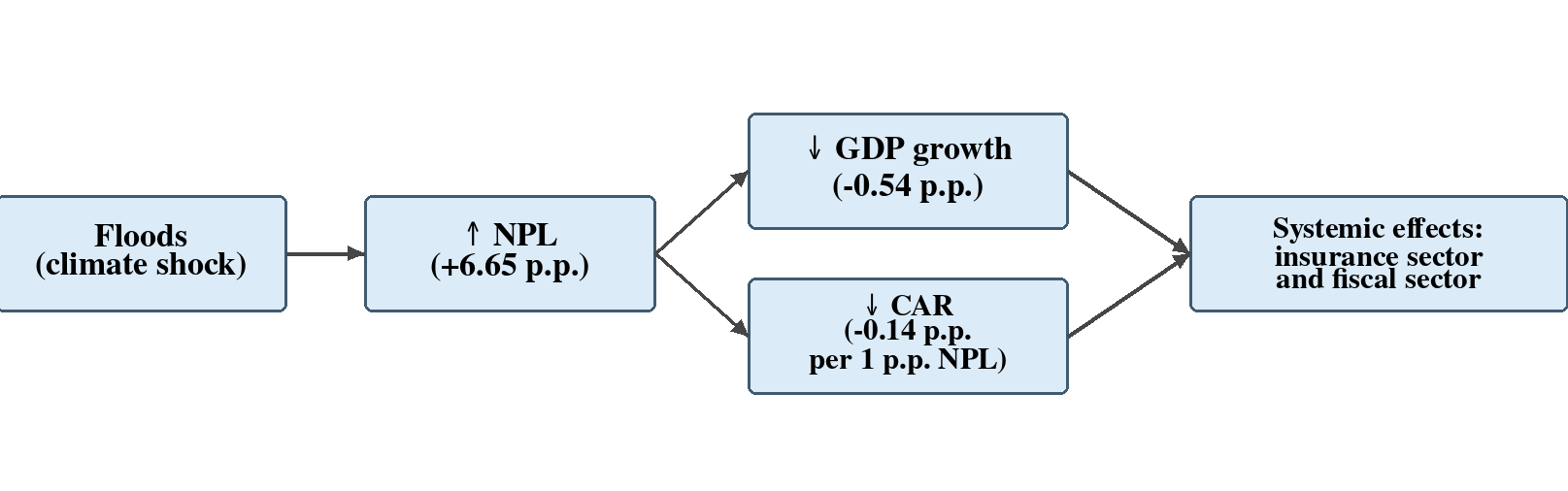

In the first part of the analysis, the finding that the 2010 flood had a statistically significant effect on the growth of NPLs (6.65 percentage points) represents key evidence of banking-sector vulnerability to extreme climate events. This result is consistent with the literature showing that physical climate risks affect borrowers’ repayment capacity through the loss of assets, income, or productive capacity (NGFS 2020; ECB 2021). In addition to confirming the relevance of climate events as a factor of financial stability, this result strengthens the argument for incorporating physical climate risks into credit-rating models and supervisory practices.

Furthermore, the finding that unemployment has a positive and statistically significant effect on NPLs, amounting to 1.57 percentage points for each one-percentage-point increase, confirms the traditional view of the macroeconomic determinants of credit risk. This is expected, since unemployment reduces household disposable income and increases the probability of delayed loan repayment. Inflation, by contrast, did not prove to be a significant predictor in this context, which may indicate a relatively limited or indirect channel through which it affects banks’ asset quality in Montenegro.

The stress test shows that a simulated climate shock in 2025 could almost double the share of non-performing loans, from 5.8% to 12.45%. This hypothetical scenario provides a basis for quantifying the potential impact on the real economy and the financial system. The projected reduction of the GDP growth rate by 0.54 percentage points in response to such an increase in NPLs illustrates the classic mechanism through which financial instability is transmitted to the macroeconomic domain.

An interesting finding, which may initially appear counterintuitive, is the negative correlation between NPLs and capital adequacy (CAR). Although one might assume that increased risk requires higher capital, banking practice points to the opposite effect: higher NPLs lead to a reduction in capital through losses and provisioning, while simultaneously increasing risk-weighted assets, thereby reducing CAR. This mechanism is fully consistent with the existing theoretical framework and the findings of previous studies (Makri et al. 2014; Hou and Dickinson 2007; Ghosh 2015). The simulation confirms that a significant increase in NPLs in 2025 as a result of a physical climate shock could substantially impair CAR, with direct consequences for banking-system stability.

Source: Created by the author

Overall, the results of this study confirm that physical climate risks, such as floods, can no longer be viewed solely as environmental issues.

Despite the relevance of the results obtained, this study has certain limitations that should be taken into account when interpreting the findings. First, the analysis is based on a relatively small sample covering the period from 2007 to 2023, which may limit the statistical power of the models and affect the stability of the estimates. Although robust standard errors and additional techniques such as bootstrap estimation were used to mitigate potential small-sample problems, the results should still be interpreted with a certain degree of caution.

Second, the operationalisation of climate risk in this paper is based on the use of a dummy variable representing an extreme climate event, namely the 2010 flood. Although intuitive and applicable under conditions of limited data availability, this approach does not fully capture the complexity and continuity of climate risks. Accordingly, the results reflect the effect of one specific event rather than the entire spectrum of climate shocks.

Finally, the model is simplified and does not include all potential channels of climate-risk transmission, such as effects on the insurance market, public finances, or international financial flows. Future research could extend the analysis by incorporating more complex modelling approaches and more detailed indicators of climate exposure.

CONCLUSION

This study provides an empirically grounded analysis of the systemic effects of climate risks on the financial stability of Montenegro, with a particular focus on the banking sector. Using a modified climate stress test, the analysis shows that an extreme climate event, in this case a flood, may have multiple effects: it may increase the share of non-performing loans (NPLs), reduce economic activity (GDP), and ultimately threaten banks’ capital adequacy (CAR). These effects are not isolated; rather, they are transmitted through the financial system, affecting the banking sector, insurance, the government’s fiscal position, and the real economy.

The model indicates that Montenegro’s financial system is sensitive to climate shocks, particularly given the country’s geographic exposure and the dominance of banks in the financial structure. At the same time, the analysis of the relationship between NPLs and CAR reveals a potentially counterintuitive finding, namely a negative association. This points to a real mechanism of pressure on capital reserves under conditions of financial stress and is consistent with the existing literature on financial stability. In this context, climate risks should be treated as an essential component of financial supervision and macroprudential policy, rather than as an external or secondary category of risk, since their consequences are evidently far-reaching and very serious.

The key recommendations arising from the analysis are as follows:

1. Institutionalise climate risks within the Central Bank

The Central Bank of Montenegro should formally integrate climate risks into its supervisory and analytical framework, including the development of climate-risk indicators and the regular application of climate stress tests adapted to the local context.

2. Establish an interinstitutional platform for climate stability

A Working Group on Climate-Related Financial Risks should be established to bring together the Central Bank, the Ministry of Finance, the Environmental Protection Agency, and other relevant bodies, with the aim of coordinating data, policies, and responses to climate shocks.

3. Improve statistics and access to climate-risk data

The lack of high-frequency and spatial data on climate events, damages, and sectoral exposure represents a serious obstacle to more precise modelling. The establishment of a national climate-exposure registry is recommended, integrating data on floods, droughts, insurance, financial losses, and risk-sensitive sectors.

Appendices

Appendix 1. NPL model including lagged values and graphical presentation of the dynamic effect

Appendix 2. Econometric output of the GDP growth-rate regression

Appendix 3. Econometric output of the CAR regression

References

- Adrian, Tobias, James Morsink, and Liliana Schumacher. 2020. “Assessing Climate-Change Risk by Stress Testing for Financial Resilience.” IMF Blog, February 5, 2020. https://www.imf.org/en/blogs/articles/2020/02/05/blog-assessing-climate-change-risk-by-stress-testing-for-financial-resilience.

- Brunetti, Celso, Benjamin Dennis, Dylan Gates, Diana Hancock, David Ignell, Elizabeth K. Kiser, Gurubala Kotta, Anna Kovner, Richard J. Rosen, and Nicholas K. Tabor. 2021. “Climate Change and Financial Stability.” FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System, March 19, 2021. https://doi.org/10.17016/2380-7172.2893.

- Campiglio, Emanuele, Yannis Dafermos, Pierre Monnin, Josh Ryan-Collins, Gertjan Schotten, and Masazumi Tanaka. 2018. “Climate Change Challenges for Central Banks and Financial Regulators.” Nature Climate Change 8 (6): 462–468. https://doi.org/10.1038/s41558-018-0175-0.

- Carè, Rosella. 2023. “Climate-Related Financial Risks: Exploring the Known and Charting the Future.” Current Opinion in Environmental Sustainability 65: 101385. https://doi.org/10.1016/j.cosust.2023.101385.

- Carney, Mark. 2015. “Breaking the Tragedy of the Horizon: Climate Change and Financial Stability.” Speech at Lloyd’s of London, London, September 29, 2015. Bank of England. https://www.bankofengland.co.uk/speech/2015/breaking-the-tragedy-of-the-horizon-climate-change-and-financial-stability.

- Chalabi-Jabado, Fatima, and Ydriss Ziane. 2024. “Climate Risks, Financial Performance and Lending Growth: Evidence from the Banking Industry.” Technological Forecasting and Social Change 209: 123757. https://doi.org/10.1016/j.techfore.2024.123757.

- Delis, Manthos D., Konstantinos de Greiff, Maria Iosifidi, and Steven Ongena. 2024. “Being Stranded with Fossil Fuel Reserves? Climate Policy Risk and the Pricing of Bank Loans.” Financial Markets, Institutions & Instruments 33 (3): 239–265. https://doi.org/10.1111/fmii.12189.

- Engle, Robert F., and Clive W. J. Granger. 1987. “Co-integration and Error Correction: Representation, Estimation, and Testing.” Econometrica 55 (2): 251–276. https://doi.org/10.2307/1913236.

- Estrada, Francisco, Miguel A. Altamirano del Carmen, Oscar Calderon-Bustamante, W. J. Wouter Botzen, Serafin Martinez-Jaramillo, and Stefano Battiston. 2024. “Assessing the Physical Risks of Climate Change for the Financial Sector: A Case Study from Mexico’s Central Bank.” arXiv preprint arXiv:2411.18834. https://arxiv.org/abs/2411.18834.

- European Central Bank. 2021. Climate-Related Risk and Financial Stability. Frankfurt: European Central Bank. https://www.ecb.europa.eu/pub/pdf/other/ecb.climateriskfinancialstability202107~87822fae81.en.pdf.

- European Central Bank. 2022. 2022 Climate Risk Stress Test. Frankfurt: European Central Bank. https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.climate_stress_test_report.20220708~2e3cc0999f.en.pdf.

- Ghosh, Atanu. 2015. “Banking-Industry Specific and Regional Economic Determinants of Non-Performing Loans: Evidence from US States.” Journal of Financial Stability 20: 93–104. https://doi.org/10.1016/j.jfs.2015.08.004.

- Imbens, Guido W., and Michal Kolesár. 2016. “Robust Standard Errors in Small Samples: Some Practical Advice.” Review of Economics and Statistics 98 (4): 701–712. https://doi.org/10.1162/rest_a_00552.

- International Monetary Fund. 2021. IMF Strategy to Help Members Address Climate Change-Related Policy Challenges: Priorities, Modes of Delivery, and Budget Implications. Washington, DC: International Monetary Fund. https://www.imf.org/en/Publications/Policy-Papers/Issues/2021/07/30/IMF-Strategy-to-Help-Members-Address-Climate-Change-Related-Policy-Challenges-Priorities-463093.

- Jessop, Simon, and Virginia Furness. 2024. “African Bank Stress Test Flags Systemic Risks Posed by Nature Loss.” Reuters, July 15, 2024. https://www.reuters.com/business/finance/african-bank-stress-test-flags-systemic-risks-posed-by-nature-loss-2024-07-15/.

- Klein, Nir. 2013. “Non-Performing Loans in CESEE: Determinants and Impact on Macroeconomic Performance.” IMF Working Paper no. 13/72. https://doi.org/10.5089/9781484318522.001.

- Louzis, Dimitrios P., Angelos T. Vouldis, and Vasilios L. Metaxas. 2012. “Macroeconomic and Bank-Specific Determinants of Non-Performing Loans in Greece.” Journal of Banking & Finance 36 (4): 1012–1027. https://doi.org/10.1016/j.jbankfin.2011.10.012.

- Makri, Vasiliki, Athanasios Tsagkanos, and Athanasios Bellas. 2014. “Determinants of Non-Performing Loans: The Case of the Eurozone.” Panoeconomicus 61 (2): 193–206. https://doi.org/10.2298/PAN1402193M.

- Messai, Ahlem S., and Fathi Jouini. 2013. “Micro and Macro Determinants of Non-Performing Loans.” International Journal of Economics and Financial Issues 3 (4): 852–860. https://www.econjournals.com/index.php/ijefi/article/view/517.

- Network for Greening the Financial System. 2020a. Guide for Supervisors: Integrating Climate-Related and Environmental Risks into Prudential Supervision. Paris: Network for Greening the Financial System. https://www.ngfs.net/en/publications-and-statistics/publications/guide-supervisors-integrating-climate-related-and-environmental-risks-prudential-supervision.

- Network for Greening the Financial System. 2020b. Guide to Climate Scenario Analysis for Central Banks and Supervisors. Paris: Network for Greening the Financial System. https://www.ngfs.net/en/publications-and-statistics/publications/old-guide-climate-scenario-analysis-central-banks-and-supervisors-2020-version.

- Network for Greening the Financial System. 2024. Scenarios in Action: A Progress Report on Global Supervisory and Central Bank Climate Scenario Exercises. Paris: Network for Greening the Financial System. https://www.ngfs.net/en/publications-and-statistics/publications/scenarios-action-progress-report-global-supervisory-and-central-bank-climate-scenario-exercises.

- Roncoroni, Andrea, Stefano Battiston, Luis O. Escobar-Farfán, and Sergio Martinez-Jaramillo. 2021. “Climate Risk and Financial Stability in the Network of Banks and Investment Funds.” Journal of Financial Stability 54: 100870. https://doi.org/10.1016/j.jfs.2021.100870.

- World Bank. 2024. Double Trouble? Assessing Climate Physical and Transition Risks for the Moroccan Banking Sector. Washington, DC: World Bank. https://openknowledge.worldbank.org/entities/publication/bc559168-cb93-445c-b70a-969a98a83024.